Is Bad Credit Costing Your Parents Thousands a Year?

One default on your parents' credit file could mean thousands in excess home loan interest every year. In 91.6% of cases, that default contains errors and can be removed.

One default on your parents' credit file could mean thousands in excess home loan interest every year. In 91.6% of cases, that default contains errors and can be removed.

Debt collectors design letters to look like court documents. Under ACCC/ASIC guidelines, that's illegal. Learn how to spot fake legal letters and what to do about them.

From demanding written communication to requesting original contracts — these four Australian consumer rights change the power dynamic with debt collectors instantly.

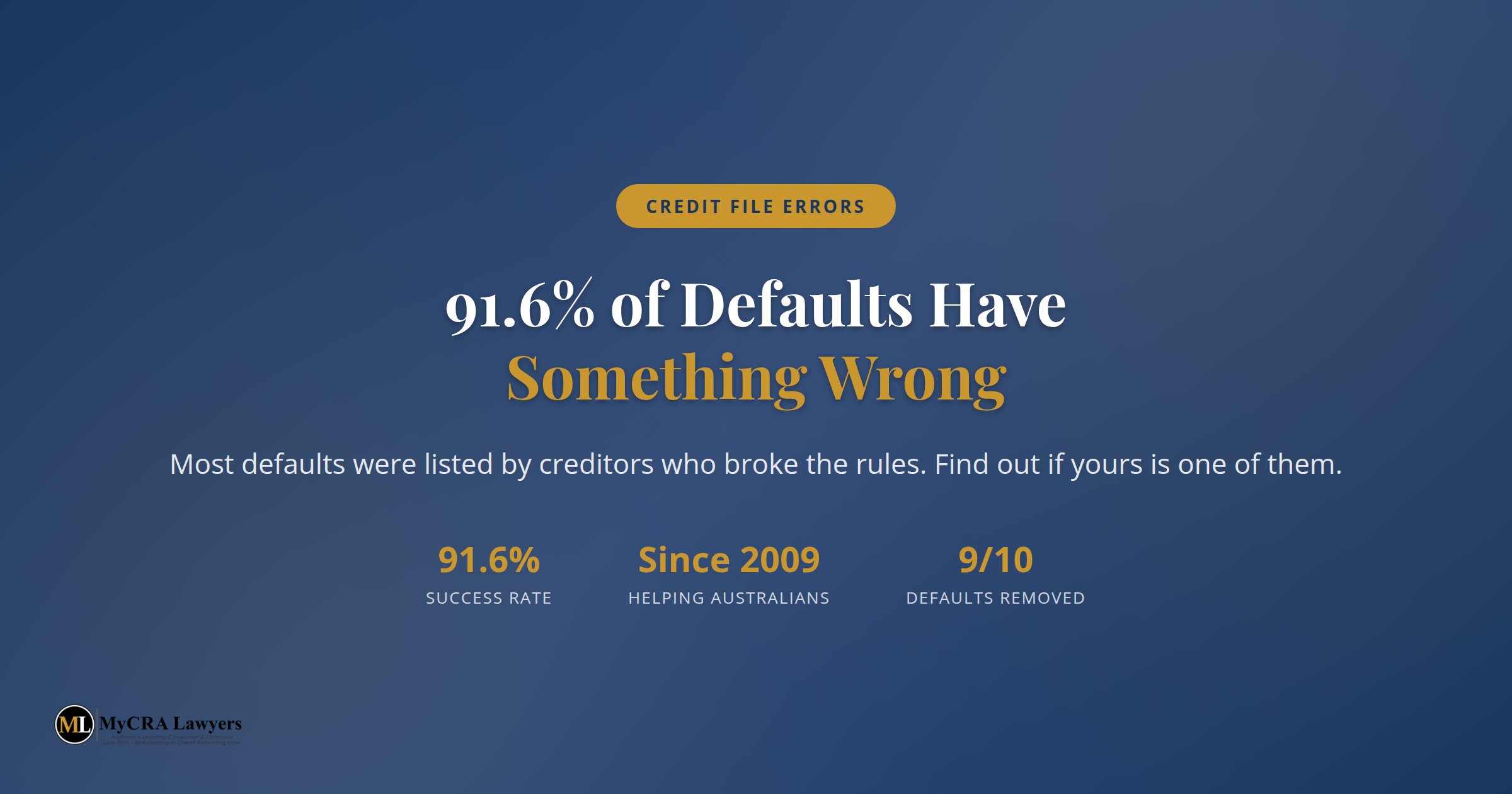

Creditors target people they think won't challenge a default. But they get the process wrong 91.6% of the time. Learn the rules they hope you never discover.

Debt collectors threatening to contact your employer is illegal under Australian law. Learn your rights under ACCC/ASIC guidelines and what to do if they've crossed the line.

An independently audited 91.6% of credit file defaults contain compliance failures. Find out if your default can be legally removed under the Privacy Act.

Debt collectors who demand you prove you don't owe a debt are lying. The burden of proof lies with them. The Federal Court confirmed it in ACCC v Panthera Finance.

The myth that checking your own credit score lowers it stops millions of Australians from finding errors. Soft enquiries have zero impact. Here's the truth.

In the Esanda case, repo agents jumped a gate, opened a garage, and pinned a debtor to the ground. The court ruled it unconscionable. Know your car repossession rights.

Real estate agents are checking credit files as part of rental applications. A default from years ago could cost you housing in today's brutal rental market.

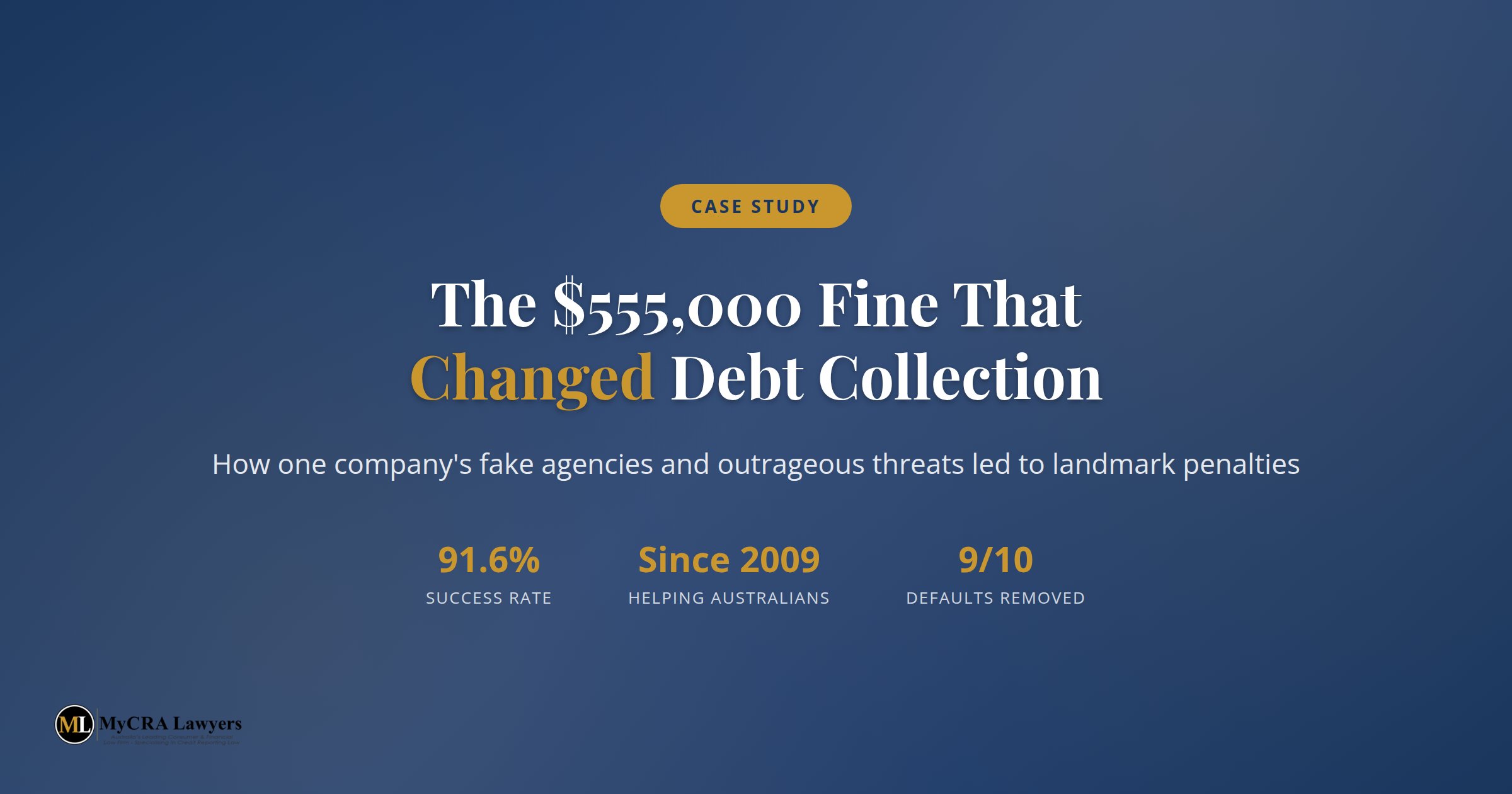

Excite Mobile created fake agencies, threatened to seize children's toys, and targeted vulnerable communities. The Federal Court fined them $555,000. Here's what happened.

Debt collectors who threaten your employment, licence, or passport are lying. The Federal Court has ruled these threats are unlawful intimidation. Know your rights.

Most credit repair advice online is dangerously wrong. Paying the debt won't remove the default. DIY letters rarely work. Here's what actually fixes your credit.

ACCC/ASIC guidelines strictly prohibit debt collectors from communicating with your children about a debt. Learn your rights and what to do if collectors cross the line.

A debt collector threatened to sell your home over a phone bill? Under Australian law, that's misleading and deceptive conduct. Learn what collectors can and can't do.